.svg "TransfixLogo-rev-tagline (1)")

The midweek market update is a recurring series that keeps shippers and carriers informed with market trends, data, analyses, and insights.

Transfix Take Podcast | Spot and Contract Rate Spread Closes to 57 cents

Transfix Take Show Notes

Jenni: Hello and welcome to an all new episode of the Transfix Take podcast, where we are performance driven. Each week we deliver news, insights, and trends for shippers and carriers from our market expert, Justin Maze.

Maze, it is always so great to be with you. What’s going on?

Maze: Glad to be back with you as well, Jenni, to talk more about the freight markets. It’s been another week and another mile driven.

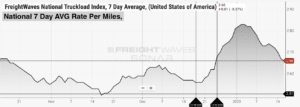

Jenni: It certainly has been, Maze. Now you know I am looking right at you for a spot market update as it is the number one topic that we have been discussing on the show since the beginning of the year.

Maze: Well, Jenni, I’m happy to tell you that we are certainly seeing some pressure relief on the spot market. As we called out last week, spot rates remained higher for a longer period of time than we had anticipated after bringing in the new year. But as we’re driving into the back half of January, we are starting to see these rates decline and even pick up speed.

Jenni: Great news for carriers that play exclusively on the spot market! But where do we see rates going? Are they the same relative to mid-December as we approach mid-January?

Maze: Well, Jenni, spot rates are still not at the levels they were at this period of time in December, but we are heading in that direction most likely within the next two weeks.

Source: FreightWaves

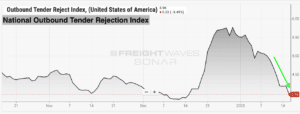

Jenni: I assume that can be attributed directly to the unexpected increase in tender rejections in the last ten days of 2022. But I would love to hear what the current state of tender rejections is right now and where that’s going to lead shippers and carriers to as we approach mid-January.

Maze: Even as rates haven’t decreased as quickly as anticipated through the last two weeks, tender rejections are a different story. Nationally, we saw them fall off a cliff last week and are now back below 4%, which means carriers are back to accepting nearly all their contract freight, closing out any gaps pushing freight to the spot market.

Source: FreightWaves

Jenni: If nothing else, Maze, that’s got to be music to shippers’ ears because that is what this battle has been over the last year: sticking to contracted freight and not bouncing it out into the spot market so that they’re not sacrificing the quality they so look for.

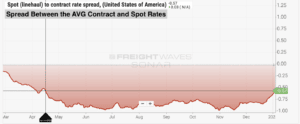

Maze: In fact, Jenni, we saw the spread between contract and spot rates close to just $0.57, but I don’t want to get into this too much as we’ll get back to this shortly.

Jenni: Yeah, hold on to it, Maze, we’ll get there in a second. I would love for you to take us through a regional breakdown of the markets. Were there any wild weather events that we weren’t expecting this time around?

Maze: That’s right, Jenni, we haven’t had any major weather events in recent days to really shift any capacity concerns. In fact, the last few weeks I’ve continued to call out how tight the Midwest was due to some weather events that took place in prior weeks. But the Midwest actually experienced a big decline in tender rejections this week. The Midwest and Northeast continue to see rates decline, with the absence of weather events, which is always good news for drivers who have to navigate weather issues more than any of us. As always, keep an eye on weather, not just for market shifts, but safety as well.

Jenni: That’s right, Maze. We want nothing more but a safe ride for all carriers to their shipper counterparts.

Maze: Let’s jump down to the South and Southeast, which saw tighter capacity through the end of 2022 and into 2023 so far. But these two regions are starting to see pricing power heavily shift in favor of shippers. These spot rates are declining faster than any other region in the country and we expect this to continue through the next week.

Jenni: OK, well now that we’re here, let’s get right into spot and contract and where they stand in relation to each other.

Maze: The volatility we have all navigated in recent weeks pushed these two rates closer together. It closed the gap to just fifty-seven cents. The last time we saw a gap this close was back in mid-April of 2022.

Source: FreightWaves

Jenni: Okay, so then that poses the question: is this gap going to continue to grow as we start seeing more of a loosening of capacity and declining of spot rates?

Maze: I think for sure it’ll definitely grow. I just do not believe that we will see it at the same level we witnessed through the period of November and December when it reached as high as $1. Spot rates without a doubt are going to continue to decline in the coming weeks, but I still believe we are close to the bottom of line haul spot rates if we get back to the levels we saw in mid-November.

Jenni: Yeah Maze, this has been your big bet for the last couple of weeks, but I’m curious to know what are your feelings on the contract side?

Maze: On the other hand, contract rates still have room to decline and we will start witnessing a steeper decline as new awards go live in the beginning months of 2023. This will keep the gap from growing to the levels we’ve seen in recent history. But this does not mean that spot rates will not continue the downward trend we are witnessing.

Jenni: Okay, so we already know that you are predicting that spot rates will bottom out, followed by contract rates in late Q2 with a slight upcycle in the back half of H2. Now, are there any other numbers that you foresee being sort of an issue or anything that we need to keep an eye on throughout the rest of the year?

Maze: Well Jenni, I believe that one of the most telling numbers that we need to keep an eye on and monitor is the net revocations of authorities or new authorities added. Net revocations continue to be high in all of the last three months of 2022 and I don’t see this trend changing just yet. Looking at new authorities, we are back down to the level we were maintaining in late 2020, early 2021. This shows that many small carriers are struggling to operate in the current market dynamics. Though this does not mean they are leaving the industry. I would assume, to be honest, that most of these drivers are just returning to operate under larger fleets during a down freight market. That isn’t an abnormal thing for drivers to do.

Jenni: And also, let’s just put to rest right now the ongoing argument whether there are enough truck drivers? Do we have a truck driver shortage? The answer is likely no because of the fact that these small owner-operators or small carriers, small fleets are moving into the larger authorities, the larger enterprise carriers. That way they can really work with contract freight as, obviously, the spot market is proving to be way more volatile than necessary to keep up with average operating costs and things like that. That said, Maze, always a pleasure hearing your insights of the week. We look forward to seeing you next week on an all new episode of the Transfix Take podcast.

Until then, drive safely.

DISCLAIMER: All views and opinions expressed in this podcast are those of the speakers and do not necessarily reflect the views or positions of Transfix, Inc. Or any parent companies or affiliates or the companies with which the participants are affiliated and may have been previously disseminated by them. The views and opinions expressed in this podcast are based upon information considered reliable, but neither Transfix, Inc. Nor its affiliates, nor the companies with which the participants are affiliated warrant its completeness or accuracy and it should not be relied upon as such. All views and opinions are subject to change.