.svg "TransfixLogo-rev-tagline (1)")

6-Month Market Outlook

July 2023 Edition

June saw a moderate bounce in trucking rates in the West and South, fuelled by the combination of produce season, the DOT week, and strong transborder produce inflows from Mexico. Bank of America’s June Truckload Demand indicators for shippers' 0-to-3-month freight demand outlook reached 49.4 before falling to 47.1, briefly approaching the 50 level, which marks the exit from recessionary territory, where the indicators have lived for 19 out of the last 21 bi-weekly surveys. Morgan Stanley’s Truckload Sentiment Survey pointed in the same direction and so did Evercore's Trucking Survey, which improved for a second straight week, to 39.3 from 37.0. Yet, while June’s trend was marginally constructive, BofA’s Transport Tracker also noted that while historically, in a muted freight environment, carriers work to cut labor costs, in the current environment, rising labor costs will likely exacerbate earnings pressure in 2H23.

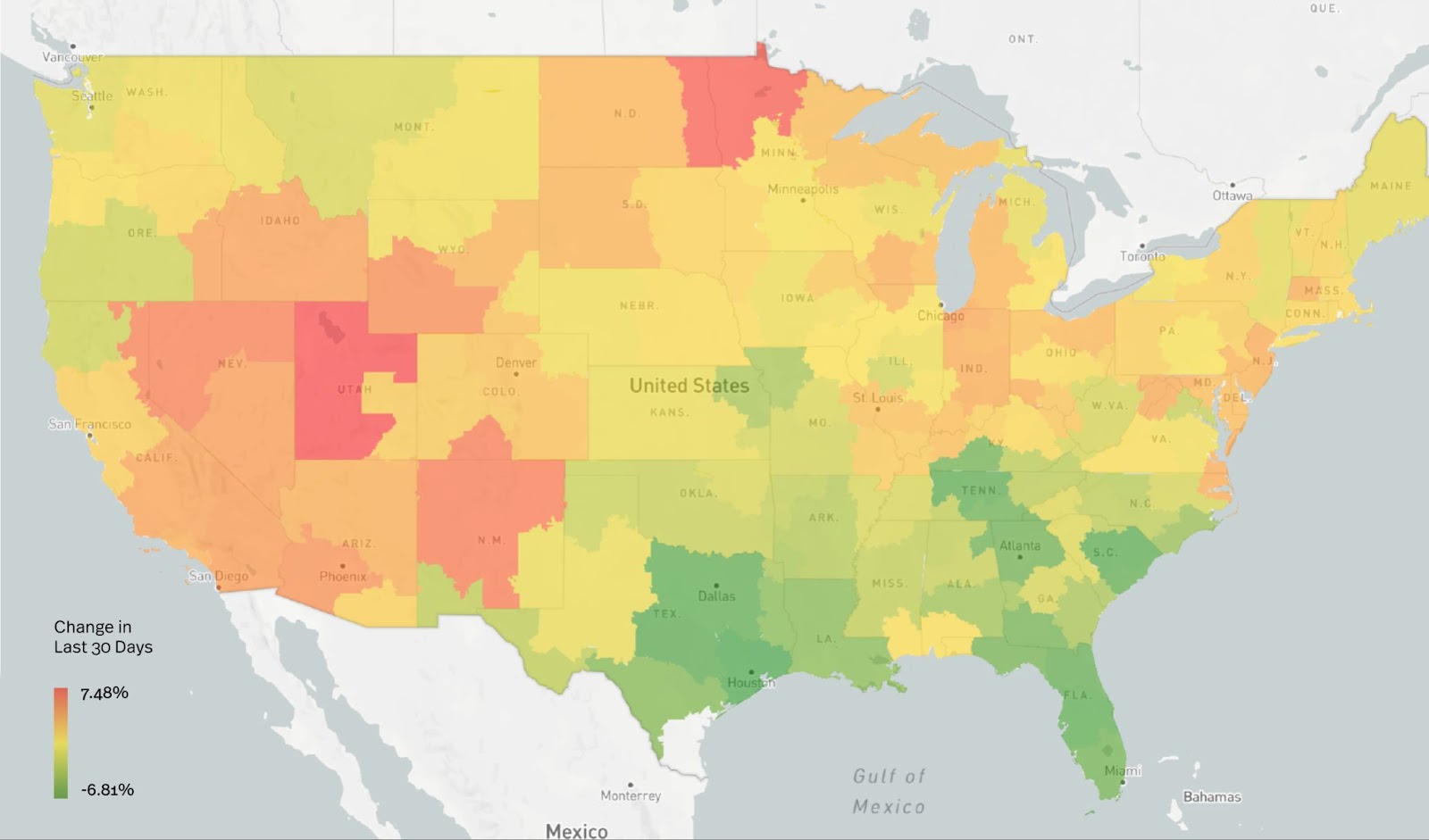

In July, Southeast rates have cooled down significantly, and, while rates in the South remain resilient, the West is already following the Southeast on the way down, as produce season pressure abates. All in all, we see more downside potential for trucking rates in the short term despite the recent improvement. June’s bounce is therefore unlikely to trigger a change in trend as more challenges for the trucking industry lie ahead. To this point, the Logistics Managers’ Index (LMI) dropped 1.7 points to 45.6 in June, the fourth consecutive drop.

Source: Transfix Internal Data

Note: As of July 17, 2023

June Class 8 net orders decreased to 176,600 units, the backlog representing about 6.3 months of production, which puts the return to a supply/demand balance at the end of 2023 or the beginning of 2024.

Additionally, our long-term mildly bearish bias for all-in rates is reinforced by market expectations of lower fuel prices going forward, with the RBOB Gasoline term structure indicating an 18% decrease in fuel prices by year-end.

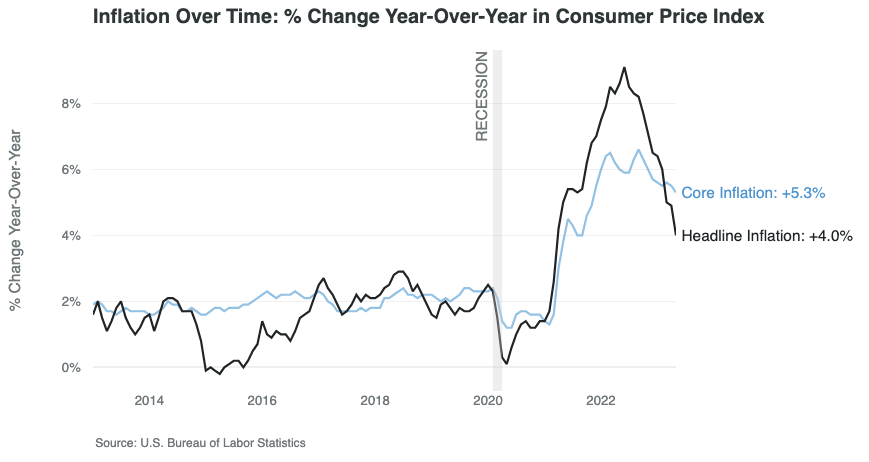

Beyond sectoral trends, the overall macroeconomic environment has offered some hope. US Inflation surprised on the downside in June, with the headline falling to 3% and Core inflation falling to 4.8%. While the Fed remains likely to hike interest rates by 25 bps in July, fixed-income debt markets are now only pricing in the July rate hike (from 2 hikes pre-CPI announcements). Yet, despite the hopes for lower future interest rates, financial conditions across the economy remain tight, and, while the job market remains resilient, the manufacturing sector continues to contract: June’s Manufacturing PMI dropped to 46.1 vs the expected 47.2, the 7th consecutive month of contraction, as Demand eased again. The factory activity gauge also contracted for the 8th month in a row, the longest streak since 2008. Consumer spending remains resilient but has to be weighed against a rapid expansion of Consumer credit, especially revolving credit.

All in all, reflecting the slight improvement in the short-term global Outlook, the likelihood of a US recession, based on the Estrella and Mishkin model for the New York Fed, has now marginally dropped from 70.85% to 67.31%. Whilst we wholeheartedly welcome the good inflation news, with Core inflation still more than double the Fed’s 2% target, and the economy continuing to soften, we are not yet seeing the end of the tunnel.

In summary, while there is some temporary consolidation in trucking rates and the odds for a cycle reversal are increasing, the overall trend remains bearish. As macroeconomic trends soften, an acceleration of trucking industry supply consolidation is increasingly likely. This could potentially result in a V-shaped trucking rate recovery down the line, but given the excess capacity, and the macro picture, such a market move is more likely to happen in Q1 2024. In the meanwhile, we anticipate more volatility and regional rate dislocations.