.svg "TransfixLogo-rev-tagline (1)")

Transfix Take Podcast | Ep. 52 – Week of May 25

Market Favor Sits with Shippers and Larger Carriers

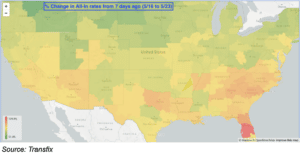

International Road Check – the country-wide 72-hour inspection blitz – threw a monkey wrench in last week’s capacity, and it was even worse than I predicted. While markets throughout the country witnessed tighter capacity starting early last Tuesday morning, the situation was felt much more acutely in the South and Southeast.

As can be expected, the inspection blitz and rise in diesel cost pressurized spot rates in most markets, but carriers weren’t able to capture adequate momentum. Shippers continued to see rate increases for freight heading into the Midwest, while the demand leaving these markets continued to drop, making it less favorable for carriers already having difficulty finding freight in the spot market. As a result, markets continue to favor shippers and larger carriers. Meanwhile, smaller carriers continue to fight the headwinds of another spike in diesel prices.

How Will Memorial Day Weekend Impact Volumes & Capacity?

Not only will capacity tighten as we approach Memorial Day, but also as we near the end of the month. These combined factors may also apply pressure on spot rates, which will benefit more carriers. Shippers should expect capacity in the South and the East Coast to remain tight but could find relief on freight destined for the Midwest as drivers head home for the weekend. Towards the end of the week, tender rejections are also likely to climb, as carriers will be more selective on freight that fits drivers’ needs to travel home. Carriers will avoid longer hauls, and shippers will face freight pile-ups from closed facilities that they’ll need to get off the dock before the end of the month.

Hot Girl Freight Summer? It’s Questionable.

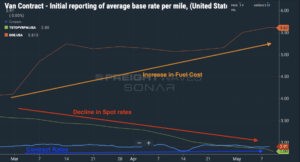

We are nearing 100 days of spot market relief. We’ve seen a spot volume decline of 18% since the beginning of the year. Needless to say, this summer will look different from the previous two. However, multiple factors could change the truckload market and create a domino effect – a concept we’ve become accustomed to since the pandemic began.

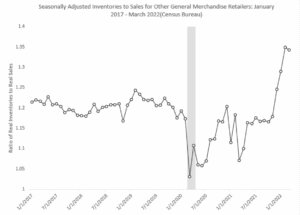

At Transfix, we get crucial insights into the supply chain pain points of large retailers. Jason Miller, logistics professor at MSU’s Eli Broad College of Business, reiterates what we’re seeing, that for two years, retailers didn’t have enough inventory to build back their inventory-to-sales ratio. Now, they potentially have too much – more inventory than before COVID-19. As inflationary pressure continues, inventory may not move as fast and retailers may need to discount sales to keep inventory from going stale. Sales could see a slight decline back to pre-pandemic levels, which could lead to a gloomy spot market.

On Friday, Journal of Commerce’s Bill Cassidy brought to industry-attention the volume of inventory still in transit to the U.S. and the potential backlog caused by COVID-19 lockdowns in China. With the current state of the economy, shippers in all industries will look to reduce transportation costs. A loosened spot market will likely cause shippers to challenge contract rates and move more freight via intermodal as demand, especially for retailers, eases.

The Impacts of COVID-19 Lockdowns in China

As the lockdowns in China continue, supply chains remain a victim. Most notably for automotive manufacturers, the lockdowns in China are intensifying an inventory shortage, putting them on the flip side of the equation that retail shippers are facing. The effects are spreading to Taiwan, a hub for global technology demand. These bottlenecks in Taiwan caused the first decline in exports in over two years.

58% of respondents in a survey conducted by Container xChange said that these lockdowns made it “hard to produce/ship as much product as planned.” Imports are a major contributor to truckload transportation and will drive how the spot market reacts in the coming months.

As quickly as the International Longshore and Warehouse Union contract negotiations started, they are now potentially being put on hold. In the coming weeks, we will welcome back Maritime Expert Lauren Beagen to dig deeper into the potential disruptions created by this delay.

The movement of freight is changing in every mode, as shippers do their best to keep up with record demand while fighting congestion at multiple points throughout the supply chain. Shippers who think forward, use data and think outside the proverbial box on solutions, while partnering with companies such as Transfix, will come out of this ongoing freight rally in a better position and well ahead of competitors. The one huge win through this pandemic has been speeding up the digital transformation of the transportation industry.

With the uncertainty and volatility surrounding the U.S. economic recovery, shippers need a partner that can help them adapt and excel — no matter the circumstance. Shippers turn to Transfix for our leading technology and reliable carrier network. As volumes drive higher, we are here to help: Learn more about our Core Carrier program and Dynamic Lane Rates. As part of our ongoing market coverage, we’ll continue to provide breaking news, resources and insight into emerging trends and the pandemic’s impact on the transportation industry.

Disclaimer: All views and opinions expressed in this blogpost are those of the author and do not necessarily reflect the views or positions of Transfix, Inc. or any parent companies or affiliates or the companies with which the participants are affiliated, and may have been previously disseminated by them. The views and opinions expressed in this blogpost are based upon information considered reliable, but neither Transfix, Inc. nor its affiliates, nor the companies with which such participants are affiliated, warrant its completeness or accuracy, and it should not be relied upon as such. In addition, the blogpost may contain forward-looking statements that are not statements of historical fact. All such statements are based on current expectations, as well as estimates and assumptions, that although believed to be reasonable, are inherently uncertain, and actual results may differ from those expressed or implied. All views, opinions, and statements are subject to change, but there is no obligation to update or revise these statements whether as a result of new information, future events, or otherwise.