.svg "TransfixLogo-rev-tagline (1)")

The Great Rate Recession Across the Country

Welcome to the week of October 18th edition of the Transfix Take! Gear up for the latest updates and trends in the trucking industry. In this issue, we're revving up with industry news, sprinting through regional breakdown highlights, and putting the spotlight on what's on the horizon for truckers.

Industry Insights: Unpacking the Road Ahead

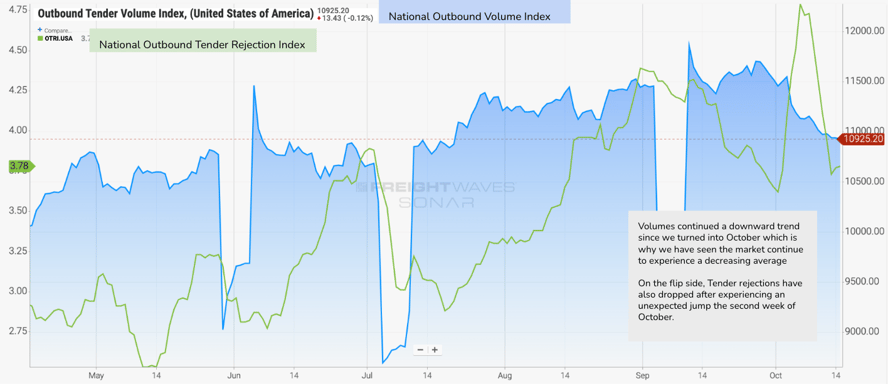

Continued Tender Turmoil: The freight industry is experiencing continued stagnation, with tender rejection rates remaining low. Last week, rejections saw a noticeable jump up, but just a week later, they dropped back below 4%, resting at approximately 3.7%. This low level of rejection rates indicates a loose market with demand unable to offset the oversupply of capacity. Volumes continue their downward trend, which we expect to change in mid-November.

Source: Freightwaves

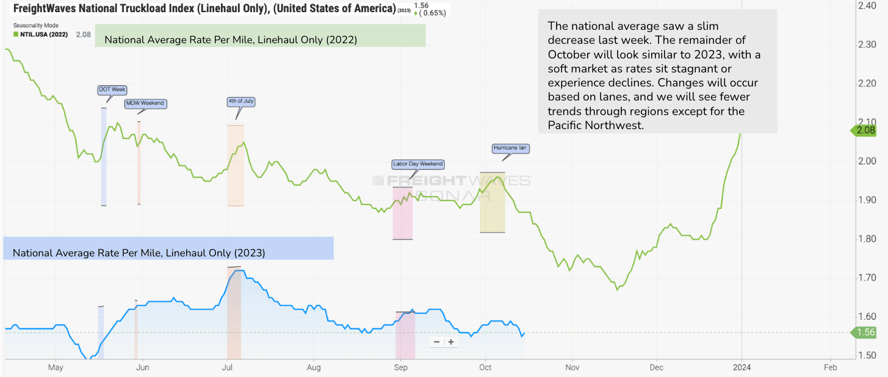

A Freight Rate Update: The national average rate per mile experienced a slight decline, currently standing at $1.56 per mile, down from $1.58 last week. The market is expected to fluctuate around this point for the remainder of October, reflecting the overall softening of the industry.

Source: Freightwaves

UAW Strike Unraveled: The United Auto Workers (UAW) strike continues, with 33,700 members striking at over 40 locations, impacting not only unionized workers but also smaller manufacturers supplying parts to assembly plants. This strike may push more supply into the spot market, affecting spot rates. However, we're not witnessing the expected tightening of the Midwest market due to the strike, as rates continue to decrease.

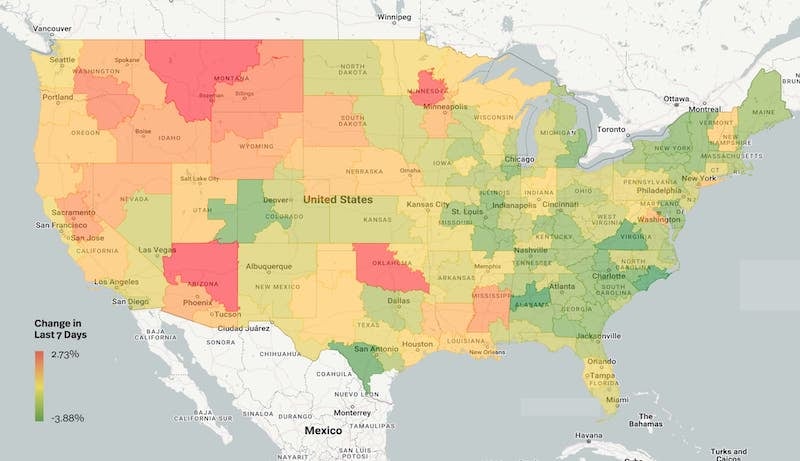

Regional Roadmap: Where the Rubber Meets the Road

Below is a regional breakdown of the freight industry, uncovering nuances and trends in various regions across the nation.

Source: Transfix Internal Data

The Midwest: The Midwest is seeing rates fall in almost every market, except for Minnesota. Despite predictions of tightening due to the potential impact of the UAW strike, the region's declining rates are not favorable to carriers.

West Coast: The West Coast remains relatively volatile compared to other regions. While the Pacific Northwest is showing signs of softening, larger volume markets in California and Arizona continue to experience fluctuations, with rates showing slight increases week over week. However, the overall trend is still downward.

East Coast: The Northeast is witnessing more significant rate declines than anticipated as it heads into the winter months. Even large outbound volume markets in this region, such as Elizabeth, New Jersey, Allentown, Pennsylvania, and Harrisburg, Pennsylvania, have experienced noticeable rate reductions. Rates are decreasing in almost every market in the Northeast, making it challenging for carriers to secure higher rates.

The South: The Southern region is struggling, with capacity outpacing demand. Rates are on the decline in nearly every market, except for Oklahoma City, Oklahoma, and Shreveport, Louisiana. Even markets like Laredo, Texas, which saw an increase until the first week of October, have experienced significant week-over-week decreases.

Southeast Region: The Southeast is seeing both colder temperatures and colder freight markets. The largest freight market in the Southeast, Atlanta, has experienced over a 2% decrease in outbound rates. Rates are declining in most markets in the Southeast, except for a few rural destinations.

Coastal Region: The Coastal region in North Carolina, South Carolina, and Virginia is witnessing a decrease in rates. Even the larger markets in this region have experienced noticeable rate reductions, making it a less favorable destination for carriers.

On the Horizon: What Lies Ahead in the Trucking Terrain

The holiday season is approaching, and carriers typically look to the spot market for higher rates during this time. However, the current soft market may impact this pattern. With rates projected to remain low and the sentiment leaning toward lower rates for longer, carriers and brokers might bid lower during the Request for Proposal (RFP) season, potentially pushing rates even lower.

We are unlikely to see the same level of volatility we experienced last year around the holidays. Nevertheless, it's crucial to keep an eye on how RFP season and supply-side shifts will influence the trucking terrain in the coming weeks.

Source: Freightwaves

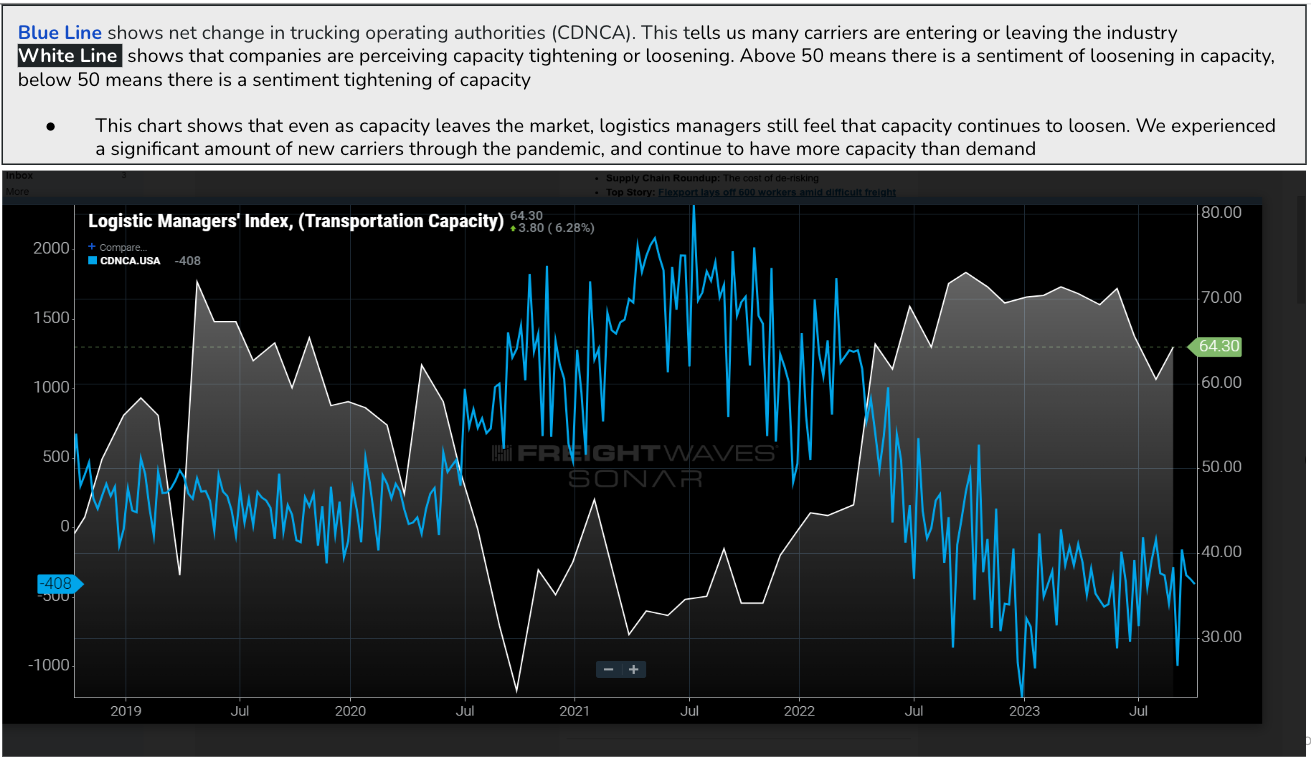

It’s also important to note the net change in trucking operating authorities–as we continue to experience a growing number of smaller carriers exiting the market. Once the market flips, we should see the greater effects in the spot market but until then, rates will continue to level out as capacity is heavily available across the country.

That's the wrap for this edition of the Transfix Take Newsletter. We'll continue to keep you in the driver's seat with the latest news, trends, and insights in the supply chain. Until the next pit stop, drive safe and stay ahead of the curve!

Drive safely!

DISCLAIMER: All views and opinions expressed in this podcast are those of the speakers and do not necessarily reflect the views or positions of Transfix, Inc., or any parent companies or affiliates or the companies with which the participants are affiliated and may have been previously disseminated by them. The views and opinions expressed in this podcast are based upon information considered reliable but neither Transfix Inc. nor its affiliates nor the companies with which the participants are affiliated warrant its completeness or accuracy, and it should not be relied upon. As such, all views and opinions are subject to change.