.svg "TransfixLogo-rev-tagline (1)")

The midweek market update is a recurring series that keeps shippers and carriers informed with market trends, data, analyses, and insights.

Transfix Take Podcast | A Nor’Easter Interrupts Premature Spring

Jenni: Hello and welcome to a brand new episode of the Transfix Take podcast where we are performance driven. It’s the week of March 15, and we are bringing you news, insights, and trends for shippers and carriers from our market expert, none other than Justin Maze. What’s up, Maze? Always good to see you.

Maze: Hey, Jenni! Great to be back with you again this week. Looking forward to diving in to reviewing last week and what we’re expecting this week, especially with the Nor’easter coming to the Northeast. I hope you’re prepared for it up in New York City.

Jenni: Well, Maze, as I recorded this episode with you, I’m looking outside of my window and see just a little bit of flurries. So not that bad. But tell me, what did you see last week when it comes to rates?

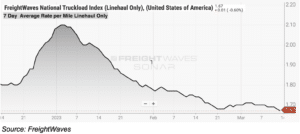

Maze: Looking back on the last week, we definitely started seeing more noticeable declines in the national average rates. The linehaul today is at $1.67 per mile. That’s down $0.03 from March 7’s $1.70 per mile.

Jenni: As a reminder, as we record this, it is Tuesday, March 14, so that rate may fluctuate based on the day that you’re listening to the podcast.

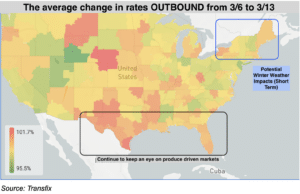

Maze: As we pointed out last week, in the South and Southwest markets, we are seeing increases being driven by produce season. That is, with the addition to weather-stricken markets throughout the West and Midwest.

Jenni: It’s interesting because last week we said we were in the clear with springtime weather. But the weather is different this week.

Maze: That’s all right, Jenni. I must have jinxed it last week, hoping that we were moving away from the winter weather, but less than a week away from the official start to spring, winter weather persists.

Jenni: My assumption is that this is going to directly impact the markets, specifically in the Northeast. But what have we got, Maze?

Maze: To turn back to the national view, we actually saw tender rejections take a turn last week. For the last couple of weeks, I’ve been calling out this slim increase in tender rejections. Well, in the past seven days, we actually saw this turn course and we are starting to see declines, mainly driven by West Coast and Midwest weather issues from the past several weeks. As the weather has started to dissipate, we are seeing tender rejections go down. Keep in mind the West Coast and Midwest are the larger freight outbound regions.

Jenni: That’s right. That becomes the driving force of that national tender rejection average going down a bit. I know you’ve got some good news on that slate, Maze. Let’s hear it. What’s going on in freight?

Maze: Everyone is getting a little relief at the pump as fuel prices continue on a downward slide. The national average diesel price continues its six week trend downward, declining nearly $0.40 per gallon from where we left January. There is some relief for carriers and shippers out there, as well as average consumers like us.

Jenni: That’s right. The last time we saw that 46-cent spread was back in October of last year. But Maze, you know what it’s time for: the regional breakdown.

Maze: Let’s dive into it. We’re going to start in the Northeast. As I stated, the Northeast is expecting a pretty significant weather event, and we will most likely see tender rejections increase in the harder hit markets in upstate New York and other parts of New England. The Northeast, as I’ve mentioned last week, is one of the regions that has the most room for declines in overall rates. This week, we will probably see rates remain stagnant, with maybe a slight increase in specific pockets that get hit harder with the weather in and around Boston and upstate New York, like Syracuse and Buffalo. But overall, I think the average for the region will stay mostly stagnant as weather dissipates, where we will then continue to see a decline in the coming weeks.

Jenni: We’ll definitely keep an eye on that. Now, what about the Midwest, Maze?

Maze: Similar to the Northeast, this region has room for downward movement, especially as we close out Q1 and head into the spring. Shippers will continue to have opportunities to push down rates, especially if it’s going into those produce markets such as the Southeast and South. But in the reverse, freight heading to the Midwest will become more difficult to cover.

Jenni: Let’s jump on down now to the Coastal region.

Maze: This region continues to be relatively flat. We are not seeing loosening or tightening. It really depends on where the freight is destined. Freight destined for the Southeast to South is likely seeing declines, especially if it’s going to south Florida. That is where we’ve seen some sizable declines. Freight going to the West Coast, of course, is still not ideal freight for carriers.

Jenni: It’ll be interesting to see when this does change, because we have seen this for the Coastal region and West Coast for quite some time now. Let’s make our way over to the Southeast region.

Maze: This is where we need to continue to keep an eye on, because southern parts of the Southeast, like Florida, south Georgia, and the panhandle, continue to see rates increase as capacity tightens. While some larger markets, like Atlanta, are actually starting to see rates stay stagnant or decline, especially if it’s going into Florida.

Jenni: Let’s head out West. Maze, are we striking gold this time or what’s going on there?

Maze: It is still no gold mine, Jenni. Rates continue to move downward after a bump due to weather, but this coming week, we’ll likely see these rates continue to fall, hitting a near bottom in the coming weeks. Moving to the South, the South is similar to the Southeast, where we are starting to see some tightening capacity around border markets, but the larger markets such as Dallas and Houston continue to be relatively loose. In the coming weeks, we expect it to play out similar to the Southeast. The border markets impacted by produce season will likely continue to tighten, pulling Dallas and Houston along with it later throughout produce season.

Jenni: As far as where we were last year around the same time at the start of produce season, some of the tighter markets, according to DAT, actually were in the Twin Falls, Idaho region, the San Luis Valley in Colorado Central and South Florida, Eastern North Carolina, Columbia Basin, Washington and Minnesota North Dakota Valley. So while we’re not exactly where we were last year, this is something that we’re definitely going to keep an eye on as we expect a more normal produce season in ’23.

Maze: That’s right Jenni. The market continues to be extremely loose from the shippers’ point of view. Carriers continue to navigate tough waters, but with the seasonality trends coming back into play, they really have the opportunity to be smart with their capacity. If they are not on contractual lanes, they need to make sure they are moving to the right markets for the right price and leaving at the right price as well. They need to pay attention to where rates and capacity are starting to shift. Again, that is, if they are not lucky enough to be on the contractual side of the market right now.

Jenni: While we’ve reached the bottom of the spot market in certain markets, namely on the East Coast, we’re starting to see that kind of level out across the nation. Is that right, Maze?

Maze: That’s right, Jenni. I still believe that we will be seeing the bottom of the spot market in the coming weeks for specific regions. However, like I called out, there are still regions that have room to decline. Also, there’s always the lanes for produce markets that may continue to see rates increase. But from a national view, it’s going to be a little bit longer. I’m not going to lie Jenni, these rates have come down farther and quicker than I would have imagined. But I do think there’s a light at the end of the tunnel for the carriers.

Jenni: How do you think carriers are going to fare within the next 60 days, Maze?

Maze: February, March, and April are big months for new RFPs to go live and it takes a couple of weeks for those to really get fleshed out. I do believe that we’re going to start seeing some relief in the spot market when all these new RFPs go live. These contract rates that carriers and brokers are getting are not going to be as lucrative as they were towards the end of 2022. Again, I cannot emphasize how important it is if you are running in the spot market, to be on top of the market and know how much and where to be sending your trucks.

Jenni: It’s why we do this market update. It’s not just for shippers. It is also for carriers to stay on top of the market each week. That said, we will see you next week with an all new episode of the Transfix Take podcast. Maze, enjoy your well-deserved vacation and until then, drive safely.

DISCLAIMER: All views and opinions expressed in this podcast are those of the speakers and do not necessarily reflect the views or positions of Transfix, Inc. Or any parent companies or affiliates or the companies with which the participants are affiliated and may have been previously disseminated by them. The views and opinions expressed in this podcast are based upon information considered reliable, but neither Transfix, Inc. Nor its affiliates, nor the companies with which the participants are affiliated warrant its completeness or accuracy and it should not be relied upon as such. All views and opinions are subject to change.