.svg "TransfixLogo-rev-tagline (1)")

The midweek market update is a recurring series that keeps shippers and carriers informed with market trends, data, analyses, and insights.

Transfix Take Podcast | What does Maze Predict for Q2?

Jenni: Hello and welcome to an all new episode of the Transfix Take podcast where we are performance driven. It’s the week of March 29 and we’re here to bring you news, insights, and trends from Justin Maze, our market expert. Maze, it is always great to be with you. What’s going on?

Maze: Hey Jenni, great to be back with you as well this week to talk about the freight markets as we start shifting gears and drive out of Q1.

Jenni: Q1 definitely had its slow start. But where do we stand now, and what are we seeing relative to the week ahead?

Maze: If you’re looking for volatility, you really have to stick with March Madness and the NCAA. Everyone’s March Madness bracket is probably broken at this point with all the upsets, but you’re not going to find much volatility in the freight market over the last seven to ten days.

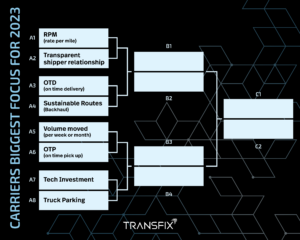

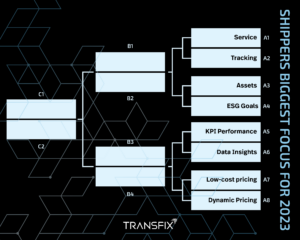

But if you want, you can join Transfix’s shipper and carrier brackets and have a little fun as well.

Jenni: That’s right. It is freight madness here at Transfix. You can check the link above to enter your bracket predictions. There’s one for shippers and there’s one for carriers. But Maze, let me know. Have there been any upsets now that we’re talking about the game of freight?

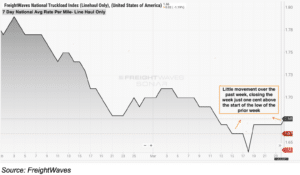

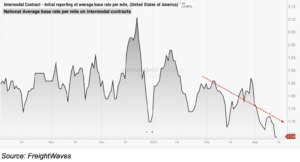

Maze: There are no upsets from what we predicted last week with the freight markets. Last week, the national average of line haul rates averaged about $1.68 per mile. That’s not much movement from the prior week at $1.67. Yes, we saw some up and down, but the last week average was $1.68. So as I stated before, there really hasn’t been much volatility.

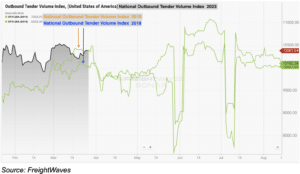

Jenni: This kind of data is what sparks the conversation: is the industry going back to pre-pandemic levels? What do you say, Maze?

Maze: Well Jenni, it looks like we’re starting to fall back into a similar market that we drove through in 2019. In fact, parts of March of 2019 had higher volumes than we witnessed this month. If this is the case, we are likely to see volume over the next two months start declining, reflecting more seasonal patterns we saw prior to the pandemic.

Jenni: Do you think lower volumes over the next two months is going to drive up rates for carriers?

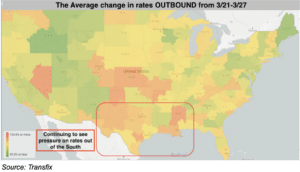

Maze: Actually, I don’t think this is going to force rates downward. I still believe that we are relatively close to the bottoming of spot markets in a few regions with other regions still having room to move down. We are still seeing some tightness in produce regions such as the South along the border in Texas and parts of southern Florida.

Jenni: So there are other external factors that are affecting the industry at the moment? Maze, I know you’ve got your finger on the pulse of what’s going on in the headlines. Let’s hear what you’re most concerned about.

Maze: A few things that catch my eye are headlines on mergers in carrier operations. These are becoming more prominent. We potentially are witnessing the largest merger in U.S. trucking history and at the same time seeing articles pop up about mid-size and large carriers ceasing operations and going out of business. Ultimately, this could start swaying the supply and demand balance. Now, I am not saying that we are anywhere near a market of volatility, but I do believe this is going to start bringing some balance to the rates and show signs of the market bottoming out on rate per mile.

Jenni: That would definitely help carriers run more profitably.

Maze: Large asset carriers have the advantage of just needing freight for their backhauls, which they are willing to accept rock bottom rates for.

Jenni: Right. What will inevitably happen is that rates will stay flat if supply continues to leave the market. But Maze, I know you’re not worried about that. I know that you think that the supply is actually pretty great right now and the market might be even considered to be loose. That said, I know that we have a diesel update. Why don’t we talk about that?

Maze: It’s always important to call out all the truck drivers out there. There is a benefit that we have been seeing not only for carriers, but shippers as well, and that is the declining price of diesel fuel. We are now at eight straight weeks of the national average diesel price per gallon declining.

Jenni: We’re moving in the right direction in terms of helping carriers maintain their expenses. I know that we’ve got a ways to go when it comes to line haul rates, which we’ll continue to keep everyone updated about. That said, you know what, it’s time for our regional breakdown. Where are we starting, Maze?

Maze: I’m going to start this week by just calling out the main points for carriers and shippers to take in. Number one, the Northeast is seeing the largest decline in rates over the past seven to ten days. This comes as capacity loosens and outbound volume falls. On the opposite side, the South region, particularly Texas, is continuing to see some tightness, most likely caused by an increase of volume brought on by produce.

Jenni: We’re likely going to see an uptick in southern produce freight as the weeks go by.

Maze: One place I want to draw everyone’s attention to is the Southeast. Now, I continue to say produce season has been tightening capacity in the state of Florida, but to my surprise, Central and Northern Florida actually saw some loosening over the past seven days. But south Florida, especially the Miami market, has continued to see some tightness with increasing rates. Out West, we are still seeing markets coming off of some inclement weather for the last couple of weeks.

Jenni: And why don’t we call out the Gulf region, Maze?

Maze: The Gulf states, as I’m sure everyone knows, have gone through some extremely severe weather the past couple of days and our thoughts and prayers are with everyone impacted. In terms of the freight market, these states are going to become very tight, inbound and outbound.

Drivers are not going to want to go out there or leave there without a premium. We will likely see more freight go in and out of these markets as recovery efforts get on their way.

Jenni: We know this is going to be more of a temporary situation as those relief efforts are underway and our thoughts are with everyone who has been affected. But Maze, why don’t we go a little deeper into these regions?

Maze: As I called out, the Northeast has continued to loosen, to be honest, past my expectations. The largest markets such as Harrisburg, Pennsylvania and Elizabeth, New Jersey are seeing the greatest loosening of capacity. Taking one lane in particular, North Jersey, to just about anywhere in Florida – we have seen rates drop close to 12% in just the last 30 days, showing how loose the Northeast is getting. Now Florida is definitely a destination where carriers want to go, so it is putting in the bad with the good, which makes it an ideal lane for a shipper to get the lowest rate possible.

Jenni: All right, and what about the Midwest?

Maze: We have still seen somewhat of a stubborn Midwest. Rates are decreasing as capacity loosens. Weather hopefully looks like it will be in the clear. I know we had some snow last week, but hopefully we continue to see beautiful weather out in the Midwest, and I really anticipate rates and capacity in the larger markets to start declining.

Jenni: Why don’t we zoom into the Coastal region?

Maze: Anywhere freight is moving out of the Coastal region, we are seeing declines, even going out West, which has been very unideal for most carriers.

Jenni: Are there any other areas in the Southeast that we should be calling out or zooming into at this point?

Maze: Georgia is easing. Atlanta became the largest market by outbound volume again last week. But even with the increased volumes, we are still seeing rates continue their downward trend.

Jenni: Okay, and why don’t we shift down to the South?

Maze: It’s no mystery that we are seeing tightening not only caused by inclement weather, but also just tightening along the border from the El Paso market to Laredo to Corpus Christi. We are seeing tightening just about everywhere in southern Texas, which is starting to leak over to Houston and the Dallas-Fort Worth markets.

Jenni: What about the West?

Maze: Weather is starting to get clearer now. There is still some snow in parts of Utah and Colorado, but overall weather is getting much better out there, and we are seeing these rates continue their downward path.

Jenni: Now Maze, we are obviously in Q2 at this point, do you have any predictions on what we could possibly see in the truckload sector over the next couple of months and anything that we should be looking out for? I know rail is top of mind, but where do you stand?

Maze: Well, Jenni, it’s a great question. If you look over at different modes of transportation like the rail, we are seeing a lot of new contracts go into place with shippers, with renegotiated rates, which is bringing down the rates on the rail. Now this is due to extremely similar conditions to the truckload side. Lower demand yields lower rates and it could eventually leak over to the truckload side of the market by shifting more longer haul freight to the rail. I don’t think it’s going to have too much of an impact as truckload rates are still at very low levels compared to the last few years.

Jenni: Always appreciate your insights, Maze. I know we don’t have many updates on the import sector. Imports are really at the same levels that we saw over the last couple of weeks. Should we see an uptick in that, we’ll definitely keep everyone updated. Until then, Maze, it’s always a pleasure.

Maze: Well, Jenni, as always, great talking to you this week. I hope everyone out there jumps onto the Transfix LinkedIn page and fills out their carrier and shipper brackets!

Jenni: Let’s see if we can create just as much buzz and volatility as the NCAA brackets did in March. Until then, everyone, we’ll see you next week with an all new episode of the Transfix Take podcast.

Drive safely.

DISCLAIMER: All views and opinions expressed in this podcast are those of the speakers and do not necessarily reflect the views or positions of Transfix, Inc. Or any parent companies or affiliates or the companies with which the participants are affiliated and may have been previously disseminated by them. The views and opinions expressed in this podcast are based upon information considered reliable, but neither Transfix, Inc. Nor its affiliates, nor the companies with which the participants are affiliated warrant its completeness or accuracy and it should not be relied upon as such. All views and opinions are subject to change.