.svg "TransfixLogo-rev-tagline (1)")

Transfix Take Podcast | Ep. 46 – Week of April 13

Produce Season Stressed by Noise at US-Mexico Border, Talks of Freight Recession

As most of the country relishes warming Spring temperatures, truckload spot markets are stuck skiing downhill. In the previous 30 days, we have witnessed tender rejections decline by over 35% and spot rates by 11%. Tender volume, rates, and rejections are all in a falling pattern, even if a bit slower as they approach a possible bottom on spot rates.

Spot rates in the Midwest and Northeast continue to see fast declines. The West Coast is currently witnessing a slow decline in rates, compared to the previous weeks. While the Southeast and South remain the “hotter” markets, rates are not increasing; they’re staying flat. This week, the border markets in Texas will likely heat up as the congestion at the border crossings clears.

What’s that Noise Coming from the US-Mexico Border?

The noise comes from more congestion – hopefully, short-lived. Almost two weeks ago, Texas Gov. Greg Abbott ramped up vehicle inspections for every northbound semi-truck. The result? Almost 25% of the trucks were cited as unsafe and put out of service, bringing the traffic flow across the border to a near standstill and causing Mexican truck exports to plummet by 80%. Protests escalated as drivers created blocked access to border crossings.

Even as secondary inspections have ended, the logjam persists and will impact the prices and availability of produce, as 43% of produce consumed in the U.S. comes from Mexico. So the next time you are grocery shopping, the price of that avocado will likely make you reach further into your pockets.

The problem goes beyond produce. According to the Association of Heavy Vehicle Producers, Mexico is the world’s number one exporter of semi-trucks and the fourth largest source of cargo vehicles.

“This affects the industry as a whole,” said Migeul Elizalde, head of the Association of Heavy Vehicle Producers. He hopes groups on “both sides of the border [will] find a quick solution and [have] commercial flows re-established to normal as soon as possible across the entire border and for all states that share a border with Texas.”

Where’s the Bottom? Are We Nearing It?

The possibility of a freight recession continues to be the talk of the industry. Where are truckload volume and rates heading? I do not believe we have seen the bottom just yet, but we could be coming upon it soon as the decline in rejections plateaus. Even as lower volumes are being seen on the spot market, overall volume remains relatively high. We are seeing more freight shift from spot to contract, causing the rapid drop in spot rates. Shippers are no longer in a rush to move freight as fast as possible, allowing them and the carrier base to run a more efficient network, positively impacting capacity usage.

Several imminent factors could change the dynamics of the current market trends.

First, produce season. Even though we kicked off the season in low gear, circumstances can always change. Traditionally, produce season brings a 20-30% volume increase to Florida, but this year it’s doubtful we’ll see any volume climbs near this level. The Southeast has seen a huge increase in volume from the ports in the past 6-10 months, which is masking the impact produce normally has in the region.

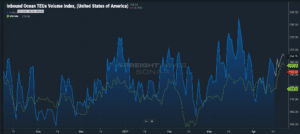

Secondly, import volumes are on the climb again (See SONAR chart below). Although China faces massive supply-chain issues that continue to compound, imports coming to the U.S. have seen an increase, which is good news for carriers. As the uncertainty within China looms and supply chain standstills persist, so do concerns over the negative impact it will have in the U.S. in months to come. Shippers will be planning ahead for back-to-school season by pulling inventory forward, but bottlenecks in China could prevent this.

After 18 months of a hectic and seemingly never ending tight freight market, the shift towards contract freight and away from spot looks sticky. While the increase of new carriers and drivers into the market over the past six months has helped us navigate unprecedented demand, most of these new entrants rely on the spot market. With declines in volume and rates alongside increased fuel costs, new entrant carriers are most at risk. Keeping an eye on the current and future market will provide an advantage over others.

The movement of freight is changing in every mode, as shippers do their best to keep up with record demand while fighting congestion at multiple points throughout the supply chain. Shippers who think forward, use data and think outside the proverbial box on solutions, while partnering with companies such as Transfix, will come out of this ongoing freight rally in a better position and well ahead of competitors. The one huge win through this pandemic has been speeding up the digital transformation of the transportation industry.

With the uncertainty and volatility surrounding the U.S. economic recovery, shippers need a partner that can help them adapt and excel — no matter the circumstance. Shippers turn to Transfix for our leading technology and reliable carrier network. As volumes drive higher, we are here to help: Learn more about our Core Carrier program and Dynamic Lane Rates. As part of our ongoing market coverage, we’ll continue to provide breaking news, resources and insight into emerging trends and the pandemic’s impact on the transportation industry.

Disclaimer: All views and opinions expressed in this blogpost are those of the author and do not necessarily reflect the views or positions of Transfix, Inc. or any parent companies or affiliates or the companies with which the participants are affiliated, and may have been previously disseminated by them. The views and opinions expressed in this blogpost are based upon information considered reliable, but neither Transfix, Inc. nor its affiliates, nor the companies with which such participants are affiliated, warrant its completeness or accuracy, and it should not be relied upon as such. In addition, the blogpost may contain forward-looking statements that are not statements of historical fact. All such statements are based on current expectations, as well as estimates and assumptions, that although believed to be reasonable, are inherently uncertain, and actual results may differ from those expressed or implied. All views, opinions, and statements are subject to change, but there is no obligation to update or revise these statements whether as a result of new information, future events, or otherwise.